This article was co-authored by Keila Hill-Trawick, CPA. Keila Hill-Trawick is a Certified Public Accountant (CPA) and owner at Little Fish Accounting, a CPA firm for small businesses in Washington, District of Columbia. With over 15 years of experience in accounting, Keila specializes in advising freelancers, solopreneurs, and small businesses in reaching their financial goals through tax preparation, financial accounting, bookkeeping, small business tax, financial advisory, and personal tax planning services. Keila spent over a decade in the government and private sector before founding Little Fish Accounting. She holds a BS in Accounting from Georgia State University - J. Mack Robinson College of Business and an MBA from Mercer University - Stetson School of Business and Economics.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, 100% of readers who voted found the article helpful, earning it our reader-approved status.

This article has been viewed 247,296 times.

One of the most challenging aspects of running a business is learning how to effectively manage your inventory so you have what your customers need and want without having too much excess, which can be a waste of money. Whether it's deciding what and how much to order, when to order, keeping an accurate count of your products, or knowing how to handle excess and shortages, knowing how to control inventory properly will help ensure your business's success.

Steps

Assessing Your Inventory

-

1Understand the goals of any inventory control system. An inventory control system should accomplish three key goals. Knowing these goals are helpful in letting you know if your current system is effective, if it can be improved, as well as how it can be improved.

- Your system should let you know what is in your inventory at all times.

- Your system should have a means of detecting and updating changes in your inventory.

- Your system should involve a plan for how much inventory to order and keep, as well as when to re-order.

-

2Invest in inventory management software. The first step to inventory control is being deeply aware of how much inventory you have on hand at any given time, what type of inventory you have available, where the inventory is located, and how it changes over time. Today, there are plenty of software applications that can assist in this process.[1]

- Be sure to spend some time searching the software market. There are extensive online reviews and analysis on all the available packages, and these reviews can let you know if the software meets your specific needs. If you are just starting, getting inventory management software that is built into accounting software. This allows you to keep all your financial information in one program, as well as coordinate it.

- Consider using Quickbooks or Peachtree. These are accounting software programs, but they also have inventory management features that can help you keep track of your inventory, and they come with a central database that can make sure all staff have coordinated information.

- POS Maid is a free inventory management software program that can be very helpful for small retail businesses.

Advertisement -

3Create clear labels. Each item in your inventory should have an item number, a quantity, and a basic description which includes the vendor name and any other important details. This makes it easy to identify precisely what the item is. For example, if you order shirts in boxes that contain 12 shirts, the box should have a label that includes the item number for the shirt, the quantity (12), and a description.

- This makes tracking easier by ensuring you know what each box contains and how much it contains.

- If you have extensive amounts of inventory, look into a barcode tracking system. This will allow you to place a barcode on each item, which allows staff to quickly scan, identify, and transfer inventory information into whatever software you are using. This is an alternative to manual labels.

-

4Perform an initial count of your inventory stock. Even if you are using software, it is important to a physical inventory occasionally. This begins by performing an initial count of your inventory stock. You will want to begin by creating a spreadsheet that has each item number, followed by columns that indicate the quantity.[2]

- You will then simply count all the available items you have, as well as their quantities.

- If you are using software, you will want to add your starting inventory to the software. You will need to add the item number, purchase information, as well as vendor. This will add the item to the software, and when you purchase inventory from now on, the software will automatically update the inventory. It will deduct from the inventory when sales are made.

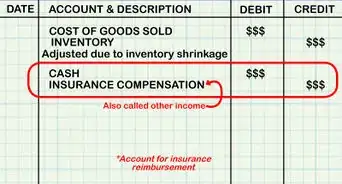

- Doing physical counts are important to ensure your software is accurate. A physical count also protects against unknown shrinkage and obsolescence.

- Inventory should be counted regularly, but can rely on statistical process or counting those items that move the most or the most valuable.

Updating Your Inventory

-

1Manually update your inventory. Inventory management software can be a helpful way to keep track of your inventory since it automatically updates your inventory records as new sales and purchases are inputted into the software. It is important, however, to have a system of manually monitoring your inventory so you have a way to cross-check the accuracy of the software (or if you opt not to use any type of software).

- You will want to pick an interval of time to regularly check your inventory by visual inspection and a physical count. This will depend on how fast your inventory moves.

- You will then want to acquire a list of any and all new inventory purchases for that time period (say, one week), as well as a list of the sales that occurred during the week (which represents inventory leaving).

- You will then take your initial inventory count sheet, and do a full count of all your inventory. Your current inventory should be equal to whatever the count last week was, minus all sales for the week, plus the new inventory purchases.

-

2Store the updated documents in an organized manner. Make sure to store your weekly checks (or whatever time period you chose) in neat folders or binders that are organized according to month. This way, if you need inventory data for a particular week, you can readily find it. It is also helpful in case your accountant needs any information.

- You will also want to cross-check the information from your manual count with whatever software you happen to be using before you opt to store it. The inventory levels in the software and from your manual check should be equal. If it is not, it is possible that improper information was entered into the software, that inventory has gone missing, or that you made a mistake during your manual count. In this case, you should re-do it.

-

3Advance to a point-of-sale (POS) inventory management method once your business size grows big enough to need a more sophisticated form of inventory control. Point-of-sale inventory control is handled, as the name suggests, at the point of sale, meaning that the cash register or computer you use for check-out at your business keeps count of your inventory. It allows you to run reports at the end of the business day, the month, the sales report period, or any other designated time frame.[3]

- If your business has a very large inventory and if many sales are made throughout a day, a point-of-sale system can allow you to track your inventory in real time. These systems are typically computers running POS software, that come with a receipt printer and cash drawer. These systems automatically update your inventory every time a transaction is made, as well as help you notify when a re-order is necessary or when supplies are running low.

- When shopping for a POS system, keep in mind that you should look for ease-of-use and basic functionality at first, and then focus on adding more advanced features as your business grows.

- You can link the POS software with your inventory management or accounting software so that every time a sale is made, your accounting software is automatically updated.

Maintaining the Right Level of Inventory

-

1Analyze sales data. The goal of inventory management is to keep up with demand, and this means that you will need enough inventory to meet whatever your projected sales are. If you have been in business for a period of time, you can use historical sales to predict approximately what your future sales will be. If you are new, you will want to base your sales forecast on the type of business you are, your location, other similarly sized businesses in your region/industry, and on any contracts or customers you have already secured.[4]

- You will want to look at how much each type of product sells on a monthly basis, and ensure you order enough inventory to cover this amount plus some extra inventory in case there is more demand than expected.

- How much extra you order depends on the nature of your business. Is your business prone to rapid increases and decreases in demand? If so, you may want to keep extra inventory to be cautious.

-

2Decide how much stock to order and keep. How much stock you keep and how much you order depends on your level of sales, the type of stock, and how much space you have available. [5]

- If your inventory consists of perishable items or if you have low levels of space, you will want to look at your previous sales data and ensure you have slightly more than that to meet projected demand plus any potential growth. Inventory management is very important if you have little space or perishable items, and you want to closely monitor levels to be sure you do not run out. You always want to choose reliable suppliers who can get you your inventory quickly and on-time.[6]

- If you have a trustworthy delivery company for your stock and they are able to deliver frequently, you can reduce your back stock.

- If your items are not perishable and if you have the space, you can consider taking advantage of bulk discounts by purchasing more inventory. This is a useful approach if your sales are hard to predict, if they fluctuate heavily, and if your products are not in a market where preferences change rapidly.

-

3Consider order and delivery times. Another factor to keep in mind is how quickly your items can be delivered to you after you order them. For instance, if it takes a week for your order of a certain item to be delivered, then you will likely want to order larger quantities of the item to have on-hand so you don't run out while you wait for the next delivery. If, however, items can be delivered the next day, then you know you can quickly replenish dwindling inventory and don't need to keep as much backstock.

-

4Choose a re-order point. Your goal is to always have enough inventory to meet customer demand, while not carrying too much inventory, as this ties up your capital unnecessarily. To make sure you have the right level of stock at all times, you need to know when to re-order.

- One approach is to specify a minimum level of stock, at which point you always re order. For example, you would never let your supply of shirts fall below 100. As soon as it does, a re-order occurs.

- This ensures you never run out. For products that move quickly, or have the potential to move quickly set a higher minimum level. If you are a seasonal business, you may want to increase this minimum level for a few months around the time of year that you see a seasonal boost.

-

5Arrange to have some "safety stock" to get you through shortages from unexpected events. For instance, if you carry items that are primarily cold-weather items, carry more of specific items needed in case of big winter weather events. This safety (or buffer) stock will prevent shortages that could occur between when you place an order and when you receive it.

- The amount of safety stock you have should depend on how prone your business is to rapid changes in demand, as well as the time of year if you are a seasonal business.

-

6Consider using an outside inventory management agency. This is especially helpful if you are a large retailer or need a good inventory count for year-end or for the end of a big sale season. The agency will count your full stock, write the reorder, and even remove unwanted merchandise to send back to the manufacturer per a predetermined arrangement with your company.

Expert Q&A

Did you know you can get expert answers for this article?

Unlock expert answers by supporting wikiHow

-

QuestionWhat is inventory turnover?

Keila Hill-Trawick, CPAKeila Hill-Trawick is a Certified Public Accountant (CPA) and owner at Little Fish Accounting, a CPA firm for small businesses in Washington, District of Columbia. With over 15 years of experience in accounting, Keila specializes in advising freelancers, solopreneurs, and small businesses in reaching their financial goals through tax preparation, financial accounting, bookkeeping, small business tax, financial advisory, and personal tax planning services. Keila spent over a decade in the government and private sector before founding Little Fish Accounting. She holds a BS in Accounting from Georgia State University - J. Mack Robinson College of Business and an MBA from Mercer University - Stetson School of Business and Economics.

Keila Hill-Trawick, CPAKeila Hill-Trawick is a Certified Public Accountant (CPA) and owner at Little Fish Accounting, a CPA firm for small businesses in Washington, District of Columbia. With over 15 years of experience in accounting, Keila specializes in advising freelancers, solopreneurs, and small businesses in reaching their financial goals through tax preparation, financial accounting, bookkeeping, small business tax, financial advisory, and personal tax planning services. Keila spent over a decade in the government and private sector before founding Little Fish Accounting. She holds a BS in Accounting from Georgia State University - J. Mack Robinson College of Business and an MBA from Mercer University - Stetson School of Business and Economics.

Certified Public AccountantInventory turnover refers to how often you buy something, sell it, and get it out of the door. It's basically the amount of time it takes you to process a sale.

Support wikiHow by unlocking this expert answer.

-

QuestionHow long should I hold inventory?Keila Hill-Trawick, CPAKeila Hill-Trawick is a Certified Public Accountant (CPA) and owner at Little Fish Accounting, a CPA firm for small businesses in Washington, District of Columbia. With over 15 years of experience in accounting, Keila specializes in advising freelancers, solopreneurs, and small businesses in reaching their financial goals through tax preparation, financial accounting, bookkeeping, small business tax, financial advisory, and personal tax planning services. Keila spent over a decade in the government and private sector before founding Little Fish Accounting. She holds a BS in Accounting from Georgia State University - J. Mack Robinson College of Business and an MBA from Mercer University - Stetson School of Business and Economics.

Certified Public AccountantIt depends on what the shelf life of the product is. If you're selling tomatoes, obviously you have to get rid of inventory really quickly. If you're selling plastic cups, you can probably store them for years. It just depends on the product and how you're storing it.Support wikiHow by unlocking this expert answer.

-

QuestionHow does inventory turnover impact profit?Keila Hill-Trawick, CPAKeila Hill-Trawick is a Certified Public Accountant (CPA) and owner at Little Fish Accounting, a CPA firm for small businesses in Washington, District of Columbia. With over 15 years of experience in accounting, Keila specializes in advising freelancers, solopreneurs, and small businesses in reaching their financial goals through tax preparation, financial accounting, bookkeeping, small business tax, financial advisory, and personal tax planning services. Keila spent over a decade in the government and private sector before founding Little Fish Accounting. She holds a BS in Accounting from Georgia State University - J. Mack Robinson College of Business and an MBA from Mercer University - Stetson School of Business and Economics.

Certified Public AccountantWell if you have a really long turnover time, you aren't processing payments quickly to get your product out. This can really damage your relationships with your customers, but it will also slow down the rate of your profit.Support wikiHow by unlocking this expert answer.

References

- ↑ http://www.entrepreneur.com/article/220631

- ↑ http://quickbooks.intuit.com/r/online-store-and-retail/basics-inventory-management

- ↑ http://www.entrepreneur.com/article/77960

- ↑ Keila Hill-Trawick, CPA. Certified Public Accountant. Expert Interview. 30 July 2020.

- ↑ http://www.infoentrepreneurs.org/en/guides/stock-control-and-inventory/#3

- ↑ Keila Hill-Trawick, CPA. Certified Public Accountant. Expert Interview. 30 July 2020.

About This Article

To control your inventory, look at your monthly sales data to work out how much product you need to buy to cover demand. If your sales figures fluctuate, try to order extra inventory to cover sharp increases in demand. Additionally, choose a minimum level of stock at which point you’ll always reorder so you don’t run out of goods. For example, you could always place a new order when you have less than 100 shirts. You could also try using accounting software with built-in inventory control features like Quickbooks or Peachtree. For tips on how to develop point of sale inventory and how to hire an inventory management agency, keep reading!