This article was co-authored by Hannah Cole and by wikiHow staff writer, Devin McSween. Hannah Cole is an Enrolled Agent and the Founder of Sunlight Tax. As an Artist and Tax Specialist with over 10 years of experience in freelance taxation, Hannah specializes in doing taxes for self-employed creative people and small businesses, setting up a business as a creative person, and personal finance issues in creative work. She has her Enrolled Agents license, which is a tax expertise and representation credential issued by the IRS. She has been hosted to speak about taxes for artists by institutions including the Harvard Ed Portal, the Boston Foundation, the New York Foundation for the Arts, RISD, and Cornell University. Hannah received her BA in Art History from Yale University, MFA in Painting from Boston University, and studied accounting at Brooklyn College.

wikiHow marks an article as reader-approved once it receives enough positive feedback. This article has 17 testimonials from our readers, earning it our reader-approved status.

This article has been viewed 1,332,429 times.

When you’re shopping for a savings account, the interest rates you’re quoted don’t take into account all the money you’ll earn. The effective interest rate does factor in how often interest is compounded each year…but how do you calculate that? Don’t worry, finding the effective interest rate is actually super easy! In this article, we’ll go over the basics of effective interest rates and give you the all the formulas you need to calculate it. If you’re ready to find how much an investment will really earn you, read on!

Things You Should Know

- The effective interest rate is higher than the nominal interest rate because it takes compounding interest into account.

- Use the formula to calculate the effective interest rate.

- For interest that compounds continuously, use the formula to calculate the effective interest rate.

Steps

Understanding Effective Interest Rate

-

1Familiarize yourself with the concept of an effective interest rate. The effective interest rate describes the full cost of borrowing. It takes into account the effect of compounding interest, which is left out of the nominal or "stated" interest rate.[1]

- For example, a loan with 10% interest compounded monthly will carry an interest rate higher than just 10%. This is because more interest is accumulated each month.

- The effective interest rate calculation does not take into account one-time fees like loan origination fees. These fees are considered, however, in the calculation of the annual percentage rate.

-

2Determine the stated interest rate. The stated (also called nominal) interest rate is the interest rate that is typically quoted to you. Think of it as the "headline" interest rate that lenders usually advertise on loans, investments, and savings accounts. The stated interest rate is expressed as a percentage.[2]

- For example, if you’re shopping for a savings account, Bank A might advertise an interest rate of 2% while Bank B has an interest rate of 3%. These are their stated or nominal interest rates.

Advertisement -

3Check the number of compounding periods for the loan. The compounding periods are generally monthly, quarterly, annually, or continuously. This refers to how often the interest is applied.[3]

- Usually, the compounding period is monthly. You'll still want to check with your lender to verify that, though.

Calculating the Effective Interest Rate

-

1Learn the formula to convert a stated interest rate to an effective interest rate. The effective interest rate is calculated using a simple formula: [4]

- In this formula, r represents the effective interest rate, i represents the stated interest rate, and n represents the number of compounding periods per year.

-

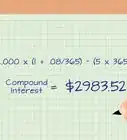

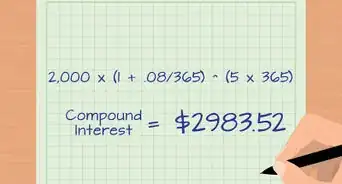

2Calculate the effective interest rate using the formula above. For example, consider a loan with a stated interest rate of 5% that is compounded monthly. Plug this information into the formula to get: r = (1 + .05/12)12 - 1, or r = 5.12%. The same loan compounded daily yields: r = (1 + .05/365)365 - 1, or r = 5.13%. Note that the effective interest rate is always greater than the stated rate.

-

3Use a different formula if interest is continuously compounded. If interest is compounded continuously, you calculate the effective interest rate using a different formula: . In this formula, r is the effective interest rate, i is the stated interest rate, and e is the constant 2.718.[5]

-

4Calculate the effective interest rate for continuously compounding interest. For example, consider a loan with a nominal interest rate of 9% compounded continuously. The formula above yields: r = 2.718.09 - 1, or 9.417%.

-

5Use a simplified method to calculate the effective interest rate. After reading and fully understanding the theory behind effective interest rates, there is a simpler way to find it:[6]

- Use the formula ((Number of intervals × 100 + interest) ÷ (Number of intervals × 100))Number of intervals × 100

- Find the number of intervals per year. A semi-annual rate is compounded 2 times each year, quarterly is 4, monthly is 12, and daily is 365.

- Multiply the number of intervals per year by 100 then add the interest rate.

- If the interest rate is 5%, for semi-annual compounding it is (2 × 100 + 5%) or 205. For quarterly it is 405, 1,205 for monthly, and 36,505 for daily compounding.

- Plug your information into the above formula to find the effective interest rate:

- Semi-annually: ((Number of intervals × 100 + interest) ÷ (Number of intervals × 100))2 × 100 = ((205)÷(200))2 × 100 = 105.0625

- Quarterly: ((405)÷(400))4 ×100 = 105.095

- Monthly: ((1,205)÷(1,200))12 ×100=105.116

- Daily: ((36,505)÷(36,500))365 ×100 = 105.127

- The effective interest is the value exceeding 100 when the principal is 100.

- The value exceeding 100 for the semi-annual calculation is 5.0625%. So, that is the effective interest rate for semi-annual. For quarterly compounding it is 5.095%, 5.116% for monthly, and 5.127% for daily.

Calculating Effective Interest Rate Glossary, Calculator, Practice Problems, and Answers

References

- ↑ http://mysmu.edu/faculty/yktse/FMA/S_FMA_1.pdf

- ↑ https://www.e-education.psu.edu/eme460/node/655

- ↑ https://www.e-education.psu.edu/eme460/node/655

- ↑ https://home.ubalt.edu/ntsbarsh/business-stat/otherapplets/CompoundCal.htm

- ↑ http://www.math.iupui.edu/~momran/m119/old/ch4h.htm

- ↑ https://eng.ucmerced.edu/people/rbales/Courses/ENGR155files/Week03/Week03_2

About This Article

To calculate effective interest rate, start by finding the stated interest rate and the number of compounding periods for the loan, which should have been provided by the lender. Then, plug this information into the formula r = (1 + i/n)^n - 1, where i is the stated interest rate, n is the number of compounding periods, and r is the effective interest rate. Solve the formula, convert your answer to a percentage, and you're finished! To learn more from our Financial Advisor co-author, such as how to calculate a continuously compounding interest, keep reading the article!