This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

This article has been viewed 117,862 times.

A fixed asset is a type of property belonging to a business that is used for production of goods and services. Fixed assets are classified as either intangible or tangible. Intangible fixed assets are non-physical properties such as a patent, copyright, and goodwill. Tangible assets include plant, equipment, land, and buildings. Accounting for fixed assets involves costs, useful life, residual value, depreciation, and amortization.

Steps

Determining Acquisition Costs and Useful Life

-

1Determine the cost of acquisition. This refers to the amount of money spent to purchase a fixed asset such as a large piece of machinery. It also includes any amounts that can be attributed directly for its improvement such as the following:

- Costs of delivery

- Costs associated with the acquisition of asset such as import duties or stamp duty

- Costs paid for preparation of asset installation

- Professional fees such as legal or architect's fees

-

2Determine the useful life of fixed asset. Useful life refers to the time period that an asset will be useful to the business (economic life), not how long it will actually last (physical life). Factors such as the age of the asset when it was acquired, how often it is used, environmental conditions, technological advancements, and the company's repair policy can affect its useful life.[1]

- Useful life refers to the period in which the asset is expected to be used that may include maintenance or repairs. It is usually less than the physical life. It can also be called economic life, average life, or effective life.

- For example, when you buy a large piece of new machinery the manufacturer may tell you it will last for 20 years. However, you know it will be used 24 hours a day outside and that there will probably be better technology available after 10 years. Therefore the machinery will most likely be useful to the business for only 10 years. Therefore, 10 years is its useful life.

Advertisement -

3Estimate the residual value of the fixed asset. Residual value is the worth or recoverable value of fixed asset at the end of its useful life. When estimated value is not of a significant amount, its value is assumed to be 0.

- Residual value is important in accounting because the book value of a fixed asset can never be depreciated to a value below residual value.

- You may also see this value referred to as "salvage value."

- For example, if you decide to replace an old piece of machinery with a new one, someone else may want to buy the old one. Its residual value is what a willing buyer would pay a willing seller, or you could look up ads for what similar pieces of used equipment are selling for on the market.

Depreciating and Amortizing a Fixed Asset

-

1Decide if you can expense an asset. To expense an assets means to immediately write it off (deduct it) as a business purchase. Direct expenses are short-term business expenditures and purchases that your company can write off immediately. These can include rent payments, purchases of raw materials that will be used in manufacturing a product, low cost computer equipment (usually less than $1,000) and office supplies.

- Some additional assets, like qualifying real estate properties, may also be expensed under IRS Section 179. This is only applicable to the types of assets currently defined under the law. For more information, see the IRS's website at https://www.irs.gov/publications/p946/ch02.html.

- Before expensing a valuable asset, consider the affect that the additional expenses will have on your earnings for the period. Compare these to the earnings impact if you decided to depreciate the asset instead.

-

2Decide to depreciate or amortize. Allocate the costs of fixed assets over their estimated useful life by using depreciation or amortization methods. Depreciation is the loss or decrease in value of tangible assets while amortization measures the decline in value of intangible assets over a period of time.

- Tangible assets that you would depreciate must have a useful life over 1 year. They include equipment, buildings and land.

- If a piece of equipment has a useful life of 10 years and you purchased it for $50,000, you can depreciate it by $5,000 per year using the straight line depreciation method. ($50,000/10 = $5,000)

- Intangible assets that you would amortize include patents, copyrights and goodwill. Goodwill refers to what you expect to gain in revenue due to your continued use of the name of a business or a product you purchase.

- Amortization is measured by dividing the cost of the fixed asset by its useful life.

- For example, you might purchase a patent for $20,000 from another company. The patent has a useful life of 10 years. You would amortize this by $2,000 per year using the straight line method. ($20,000 / 10 =$2,000)

-

3Choose a depreciation method. The most common method used for depreciation is the straight-line method. It is calculated by dividing the purchase price of a fixed asset and dividing it by its useful life. The result is then subtracted from the value of the asset at the end of each year and recorded as depreciation expense.[2]

- For example, $50,000 purchase price/10 years useful life = $5,000. That would mean that the value of the asset at the beginning of year 2 would be reported as $45,000 ($50,000 - $5,000). $5,000 in depreciation expense for the asset would be recorded in year 1.

- Other methods of depreciation can be used such as sum-of-the-years-digits method, declining balance method, and units-of-production method.

-

4Consider the sum-of-the-years-digits-method (SYD). This is used if an asset depreciates faster in the earlier years than it does as it gets older. For example, a car would depreciate more in the earlier years of ownership. The formula to use is SYD = n(n + 1)/2 where n = estimated useful life.

- If the useful life is 5 years, the SYD is 15. Then take the number of years of estimated life remaining at the beginning of each year and divide by the SYD of 15. For example, 5/15, 4/15, 3/15, 2/15 and 1/15. Apply these percentages to the value of the fixed asset each year to determine the depreciation amount.

- 5/15 = 33.33% or .3333. If the value at year 1 is $90,000, multiply this by .3333 = $29,997 depreciation.

- For year 2, again use the value of $90,000 for the asset. 4/15 = 26.66% or .2666. $90,000 x .2666 = $23,994 depreciation for year 2. Continue this pattern for years 3, 2 and 1.

- If the useful life is 5 years, the SYD is 15. Then take the number of years of estimated life remaining at the beginning of each year and divide by the SYD of 15. For example, 5/15, 4/15, 3/15, 2/15 and 1/15. Apply these percentages to the value of the fixed asset each year to determine the depreciation amount.

-

5Consider the declining balance method. This is used when an asset is depreciated even faster in the earlier years than you would use for the sum-of-the-years method. Large computer equipment where the technology frequently goes out of date would be an example of when you would use the declining balance method.

- To calculate, let's say a piece of equipment has a useful life of 10 years. Divide 1 by the number of years of useful life, 1/10 = .1. Next multiply this rate by 2 to get 0.2. Apply this rate to the declining book value of the machinery. This is referred to as "double-declining balance depreciation."

- For example, for an asset worth $100,000 with a useful life of 10 years, you would calculate depreciation in the first year by multiplying the value by the declining balance multiple, which is 0.2, to get $20,000. So, the depreciation expense in the first year is $20,000 and the value of the asset in year 2 is $80,000.

- This continues in year 2 the same way. Multiply the current value, $80,000, by 0.2 to get the new depreciation expense, $16,000. Deduct this expense and get the asset starting value for year 3, $64,000.

-

6Consider the units of production method. This is based on the number of parts produced by the asset rather than a period of time. In a year when many units are produced the depreciation amount will be higher.[3]

- To calculate, let's say a piece of machinery has a value of $60,000 and is projected to produce 10,000 units over its useful life. First, find the depreciation per unit by dividing $60,000 by10,000, totaling $6 per unit. Then determine the depreciation expense for a specific period of time based on how many units were produced. If 2,000 units were produced, multiply this by the per unit depreciation amount = 2,000 * $6 = $12,000 depreciation expense.

Reporting Fixed Asset Values

-

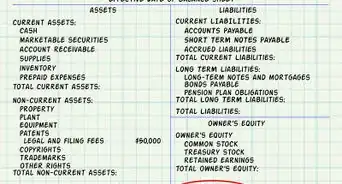

1Record the values of intangible and tangible fixed assets. These will be entered in the company's balance sheet under the category "non-current assets" or "fixed assets" at the end of an accounting cycle. An accounting cycle can be monthly, quarterly or annually.

-

2Keep all backup documentation. This can include invoices, depreciation logs, maintenance reports, professional fees related to the asset, etc. Records should be kept for seven years and will be needed for future audits.

-

3Document all internal controls. This includes written policies and procedures for acquiring assets, determining their value, depreciation methods and the name of the positions of people that are responsible (general accounting manager, accounts payable manager, chief financial officer, etc.) These will also be needed for an audit.

References

About This Article