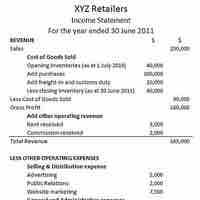

Income statement is a company's financial statement that indicates how the revenue is transformed into the net income.

The income statement, or profit and loss statement (P&L), reports a company's revenue, expenses, and net income over a period of time.

Noncash items, such as depreciation and amortization, will affect differences between the income statement and cash flow statement.

The primary purpose of the income statement is to assess efficiency as revenues transform into profits/losses.

Income statements have several limitations stemming from estimation difficulties, reporting error, and fraud.

GAAP's assumptions, principles, and constraints can affect income statements through temporary (timing) and permanent differences.

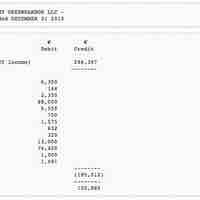

A balance sheet reports a company's financial position on a particular date.

The balance sheet relationship is expressed as; Assets = Liabilities + Equity.

The balance sheet of a business provides a snapshot of its financial status at a particular point in time.

Balance sheets are prepared with either one or two columns, with assets first, followed by liabilities and net worth.

Cash, receivables, and liabilities on the Balance Sheet are re-measured into U.S. dollars using the current exchange rate.

Assets on a balance sheet are classified into current assets and non-current assets. Assets are on the left side of a balance sheet.

The balance sheet contains details on company liabilities and owner's equity.

Liquidity, a business's ability to pay obligations, can be assessed using various ratios: current ratio, quick ratio, etc.

Working capital is a financial metric which represents operating liquidity available to a business, organization and other entity.

The debt-to-equity ratio (D/E) indicates the relative proportion of shareholder's equity and debt used to finance a company's assets.

Book value is the price paid for a particular asset, while market value is the price at which you could presently sell the same asset.

The three limitations to balance sheets are assets being recorded at historical cost, use of estimates, and the omission of valuable non-monetary assets.

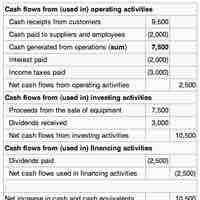

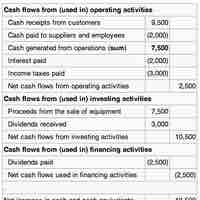

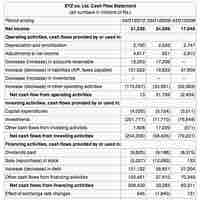

A statement of cash flows is a financial statement showing how changes in balance sheet accounts and income affect cash & cash equivalents.

The cash flow statement has 3 parts: operating, investing, and financing activities. There can also be a disclosure of non-cash activities.

Cash flows from financing activities arise from the borrowing, repaying, or raising of money.

Cash flow from investing results from activities related to the purchase or sale of assets or investments made by the company.

The operating cash flows refers to all cash flows that have to do with the actual operations of the business, such as selling products.

Having positive and large cash flow is a good sign for any business, though does not by itself mean the business will be successful.

The statement of cash flows is a useful tool in identifying organizational liquidity, but has limitations when it comes to non-cash reporting.

Merchandising is any practice which contributes to the sale of products to a retail consumer.

In merchandising accounting, purchases are the amount of goods a company buys in the course of a year, including the kind, quality, quantity, and cost.

Net sales are gross sales minus sales returns, sales allowances, and sales discounts.