This article was co-authored by Samantha Gorelick, CFP®. Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

This article has been viewed 36,900 times.

Creating a budget, while admittedly not the most exciting project in the world, is a great way to take control of your financial life. When you know how much money you have coming in and going out, you can make smarter financial decisions. Estimating your total weekly income and expenses is a great starting point. Look for ways to save, such as cutting down on eating out. Coming up with a set of budgeting goals, like saving for a down payment on a dream house, will help to keep you motivated. You can do this!

Steps

Establishing a Budget Framework

-

1Gather all of your paperwork. Before you sit down to make your budget, either print out or electronically find any financial documentation from the past six months. This includes any bank or savings statements, pay stubs, loan statements, monthly bills, and store receipts.[1]

- As soon as you decide that you are going to create a budget, start putting aside receipts instead of shredding them.

-

2Calculate your weekly income. Write down all of your sources of income for an entire month. If your income tends to vary a great deal, then add together the past three months and divide that number by three to get a monthly average. To get a weekly income number, take your monthly average and divide it by four.[2]

- For budgeting purposes, only include your work income after-taxes, as shown on your pay stubs.

Advertisement -

3Make a list of all of your expenses. Get a pen and paper or use a budgeting program, such as Mint, and tally all of your expenses over the past month. Divide all of these expenses into thematic categories, such as dining out, groceries, and gas. Then, total the amount spent over the month and divide it into four to get the weekly amount. Do the same thing with monthly bills, such as water, electricity, or your phone.[3]

-

4Divide your expenses into discretionary and non-discretionary. Discretionary expenses are ones that stem from lifestyle choices made by you, such as eating our or gym memberships. These expenses should amount to no more than 30% of your total income. Non-discretionary expenses are necessary ones that you can only alter slightly, such as rent or a mortgage payment. They should amount to 50% or less of your total income each month.[4]

- This step should give you an idea as to whether or not you are spending too much on discretionary items, like eating out. It will also tell you whether or not your current cost of living, including expenses like a mortgage, is too high for your income.

-

5Subtract your expenses from your income. Add up your weekly expenses from both your discretionary and non-discretionary categories and subtract this amount from weekly income. If you have money left behind, put it toward savings or meeting your other goals. If you break exactly even, then you have no excess income. If you end up with a negative number, then you need to make some serious budget adjustments.

- Be sure to set aside enough money each week for all of your fixed expenses, including your rent or mortgage, utilities, and online subscriptions. Then, whatever's left over is the money you can use for discretionary spending, whether that's buying food, going shopping, or putting money into your savings.[5]

-

6Make any necessary spending adjustments. If you are striking even or spending too much each week, look to your discretionary expenses as a way to cut costs. Scrutinize each purchase to determine if it was absolutely necessary. Play with the numbers to determine how much you would need to cut back in a certain category to see the savings you desire and to get you back into a positive income-expense ratio.[6]

- For example, a financial weak point could be eating out too frequently when meals at home could save you money.

Creating Budget Goals

-

1Write down how you envision your financial future. This is less about creating specific goals and more about being realistic regarding what kind of lifestyle you want moving forward. Do you plan to make major investments, like purchasing a house, or would you like to use your funds for travel? Do you want to accumulate your wealth in savings or establish a safety fund and then spend as you like? Do you need to support others with your funds?[7]

- Some people find that cutting out images of what they consider a financially successful lifestyle to look like, such as a photo of a vacation home, helps to motivate them and keep them focused.

-

2Calculate your total assets. Add together any monies that you currently have in checking or saving accounts, any interest or capital in retirement funds or investments, and the adjusted value of any major property, like a car or home. Knowing this amount may not seem important, but it lets you know how to set realistic goals that apply to your entire financial well-being.

-

3Create a list of short-term goals. These are goals that can be realistically accomplished in under a year. Brainstorm a list of all possible options and sort them according to priority and cost. Then, decide which ones you can start to work on based upon the available funds in your budget.[8]

- For example, you might want to save up $3,000 for an emergency fund. Divide this up by the amount that you can set aside for it each week while staying in your budget.

-

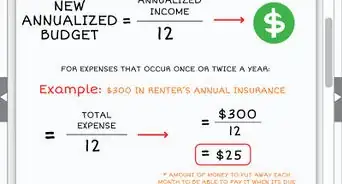

4Make long-term financial goals. Look for ideas that will take over a year and closer to 5-10 years to complete. This could mean purchasing a home or even increasing retirement savings. Estimate when you would like to achieve each goal and attach a monetary value as well. Then, divide the monetary value by the number of weeks it will take. This is the amount that you’ll need to set aside for your particular long term goal.

- For example, imagine that your goal is to save $30,000 for retirement over the next five years. There are 52 weeks in a year. Divide 30,000 by 260 (52 weeks times 5 years) and you’ll need to save $115 extra each week to make this happen.

-

5Enter your goals into the budget as expenses. Decide which financial goals you’d like to target first. It’s often best to start small. Plug the amounts that you’ll need to save each week for your goals into your budget and see if it is still doable and realistic.[9]

- For example, your budget may currently show that you have only $200 free for goal savings each week. Then, you will need to find goals that fit under that amount, such as putting aside $50 a week for an emergency fund.

- This is an important step because it takes your goals out of an illusion and into reality. It also helps to ingrain a habit of saving, instead of spending.

Making Smart Financial Choices

-

1Schedule a weekly budget planning session. A budget is a constantly changing thing and requires continual monitoring and updates. Set a day and time each week when you’ll sit down, look over your budget numbers, and make any necessary adjustments.[10]

- As you look over your budget, make sure to update your expenses by including any discounts that you’ve been able to negotiate.

-

2Contact companies for bill reductions. Reach out to all of the companies who you are paying regularly and inquire about any cost savings programs or discounts. You may qualify for a program that you’ll otherwise know nothing about. If you’ve been a customer for a long time and pay your bills on time, tell the representative.

- For example, your phone company may be able to switch you over to a promotional rate in order to keep your business.

- As always, when talking with customer service representatives, try to stay friendly and focused. If you get too frustrated, just thank them, hang up, and call back later.

-

3Use a spending or bill payment tracking app. There are many budget applications, such as BillGuard or Dollarbird, that you can use on your phone, computer, or both. Experiment with which one is the best for you, as some charge a fee while others are free. Make sure to reliably enter data into the app, as it will only be as helpful as the information you give it.

- You might even consider using a bill payment application to keep your payments on time and to show you how your bill amounts change over time.

Expert Q&A

-

QuestionHow do I make a weekly budget spreadsheet?

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Financial PlannerLook at your bank and credit card statements, or write down everything you buy if you use cash, to get an idea of what you're spending. If you build your budget around how you actually spend money, it will be much easier to stick to, even if you need to make adjustments later on. -

QuestionHow do I stick to a weekly budget, even when it's hard?Samantha Gorelick, CFP®Samantha Gorelick is a Lead Financial Planner at Brunch & Budget, a financial planning and coaching organization. Samantha has over 6 years of experience in the financial services industry, and has held the Certified Financial Planner™ designation since 2017. Samantha specializes in personal finance, working with clients to understand their money personality while teaching them how to build their credit, manage cash flow, and accomplish their goals.

Financial PlannerThe easiest way to stick to a budget is set aside the money you need each week to pay for your monthly fixed expenses. That includes your rent or mortgage, your utilities, your online subscriptions, and everything else you get charged for on a monthly or bi-monthly basis. Then, that leaves what's left for discretionary spending. You can use that for buying food, going shopping, or putting money into your savings.

Warnings

- It’s normal for budgeting to take quite a while, at least the first few times. Just try to be patient and keep the information as detailed as you can. Feel free to take a break and come back to it if you need to.⧼thumbs_response⧽

References

- ↑ http://www.pennypinchinmom.com/how-to-create-a-budget-beginner/

- ↑ http://nataliebacon.com/how-to-create-budget/

- ↑ http://nataliebacon.com/how-to-create-budget/

- ↑ https://www.forbes.com/sites/laurashin/2016/02/29/how-to-budget-a-simple-flexible-method-for-everyone/#731bacd25881

- ↑ Samantha Gorelick, CFP®. Financial Planner. Expert Interview. 6 May 2020.

- ↑ http://nataliebacon.com/how-to-create-budget/

- ↑ http://nataliebacon.com/how-to-create-budget/

- ↑ http://nataliebacon.com/how-to-create-budget/

- ↑ http://nataliebacon.com/how-to-create-budget/

About This Article