This article was co-authored by wikiHow Staff. Our trained team of editors and researchers validate articles for accuracy and comprehensiveness. wikiHow's Content Management Team carefully monitors the work from our editorial staff to ensure that each article is backed by trusted research and meets our high quality standards.

There are 9 references cited in this article, which can be found at the bottom of the page.

This article has been viewed 359,498 times.

Learn more...

The US Treasury produces two types of savings bonds: Series EE and Series I. Series EE bonds, sometimes called Patriot Bonds after 2001, differ from Series I because they are guaranteed to double in value after 20 years. They are meant to be a long-term, low-risk investment and are available in any amount from $25 to $10,000. They are granted in 30-year terms, but can be cashed in at almost any point in their lifespan. Cash in your electronic bonds easily online through the TreasuryDirect website. If you have a paper savings bond, you can redeem it at your local bank. You can also cash in lost, damaged, or stolen bonds by mail.

Steps

Redeeming Your Bond

-

1Decide how much of the bond you want to redeem. For electronic bonds, you have to cash in a minimum of $25. If you redeem only a part of your bond, you must leave at least $25 in your account. For paper bonds, there is no limit to value you can redeem.[1]

- Your bank might have a policy on how much of your paper bond they will redeem in one transaction.

- If you have individual paper bonds, they cannot be split. Each bond must be redeemed in full.

-

2Redeem an electronic bond online. Electronic bonds can be redeemed online and credited directly to a checking account within 1 or 2 days. Simply go to https://www.treasurydirect.gov/ and redeem your bonds in your account.

- If you don’t have a TreasuryDirect account, click “Open an Account” on their homepage. You will need your social security number or Employer Identification Number, a valid email address, a US address, and your bank account number and routing number.

Advertisement -

3Take your paper savings bonds to the bank. Check with your local bank to see if they redeem EE savings bonds. If they do, be sure to find out if they have a dollar limit on redemptions. Ask what identification or other documents you will need to bring with you.[2]

- If your bank won’t redeem your paper bonds, look up the local Federal Reserve bank in your area and contact them for instructions on how to redeem them.

- Note that the policies about redeeming bonds less than and greater than $1,000 in person may differ. Paper bonds greater than $1,000 may require a certifying officer to be with you when you cash in the bond.

- You can also convert your paper bonds into electronic bonds online at http://www.treasurydirect.gov/BC/SBCPrice. Set up an account and login. Then click “Manage Direct,” and then “Establish a Conversion Linked Account” in the “Manage My Linked Accounts” menu. Click “Create Account” and follow the instructions.[3]

-

4Redeem lost, stolen, or destroyed bonds by mail. If you no longer have your paper bonds, you can still cash them in. Fill out TreasuryDirect’s Form 1048 at https://www.treasurydirect.gov/forms/sav1048.pdf. Be sure to include as much information as possible about your bond (names of the owners, social security numbers, date issued, dollar amounts, serial numbers, etc.). You will need to sign the document and have it certified by a certifying officer at your local bank or credit union.

- Mail the form to:

Treasury Retail Securities Site

PO Box 214

Minneapolis, MN 55480-0214.[4] - If you are in an area that’s been affected by a disaster, you only need to complete parts 1, 5, 6.B. and 7. Be sure to write “Disaster” on the top of the form’s first page and on the envelope.[5]

- If you are outside the US, you can have your form certified at a US embassy or consulate, by an American bank branch, or by a notary public who is certified by a US diplomatic or consular office.[6]

- Mail the form to:

-

5Have proof that you are entitled to the bond if you aren’t listed as the owner. Whether you cash in the bonds online or in person, you will need to prove that you are entitled to the bond. If the owner has died and you are listed as a survivor on the bond, you will need to present a copy of the death certificate and proof of your identity.[7]

- If you are redeeming a paper bond and you are named the survivor, be sure to call the bank before you go in to clarify what documents they require.

- If there are no survivors named on the bond, the bond goes into the estate of the deceased owner.

- If the bonds in the deceased owner’s estate total more than $100,000, the court system will administer the estate and reassign the bonds to new owners.

- If the bonds in the deceased owner’s estate equal less than $100,000 and no court is involved, request ownership of the bond(s) by filling out FS Form 5336 at https://www.treasurydirect.gov/forms/sav5336.pdf, sign it in the presence of a certifying officer, send the bond and the form to:

Treasury Retail Securities Site

P.O. Box 214

Minneapolis, MN 55480-0214

-

6Be prepared to pay taxes on your EE savings bond. You have the option of deferring taxes until you cash the bond in, or paying taxes when the bond matures — whichever comes first. If you do not wish to defer taxes, you may pay them at the end of the year.[8]

- If you wish to factor in an education tax credit, it's best to defer taxes until you cash the bond in.

-

7Use bonds issued after 1989 for education to get a tax break. Although you usually must pay taxes on the interest you earned on your savings bonds, you may be eligible for an exemption if you use the money for higher education expenses.[9]

- These expenses include tuition, books, and other supplies directly related to your education.

- The owner of the bond must be 24 years old before the issue date of the bond, so parents who buy bonds to pay for their child’s education should put the bond in their own name and list their child as a beneficiary (and not a co-owner). That also means if you are using a bond to pay for your education, you will only be exempt from tax if the bond is in your parents’ name.

Deciding When to Cash In

-

1Cash in after the mandatory 1-year period unless you’ve been affected by a disaster. Whether you purchased the bond yourself or were given the bond as a gift, it normally cannot be redeemed until 1 year after its purchase. If you live in a federally-declared disaster area, the 1-year waiting period can be waived.[10]

- If you are cashing in electronic bonds for disaster relief, simply write an email inside your TreasuryDirect account at https://www.treasurydirect.gov/ explaining the situation.

- If you’ve been affected by a disaster and are cashing in paper bonds, your bank should be able to waive the 1-year minimum holding fee if you live in a federally-declared disaster area.

-

2Avoid penalties by waiting at least 5 years to cash in your bonds. EE savings bonds were meant to be long-term investments. If you cash in your EE bond before it is 5 years old, you will lose the last 3 months of interest.[11]

-

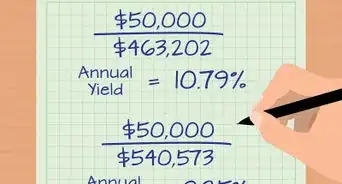

3Wait at least 20 years for the best investment on a paper bond. Paper EE savings bonds double in value at the 20-year mark, meaning that if you want to get the best bang for your buck, wait until the bond has reached its 20-year maturity.[12]

- Say you have a bond worth $100 and an interest rate of 0.20%. After 20 years, the bond reaches a maturity value of $200, even though the nominal value of the loan, given the interest rate, would normally be $105. After the adjustment, and until the loan hits 30 years old, it will earn a fixed interest rate.

- Regardless of the interest rate on your current EE savings bond, waiting 20 years before cashing in the paper bond will guarantee you an effective yield of about 3.5 percent.[13]

-

4Cash in any EE savings bond that is older than 30 years old. EE savings bonds only earn interest for 30 years. If you have a bond that is older than 30 years, it doesn't make much sense to keep it invested in an interest-less bond, so cash it in.[14]

-

5Find out the interest rate of your EE savings bonds. Knowing the value of EE savings bonds will help you decide whether it's a good idea to cash in your bonds. Depending on the year issued, EE savings bonds have various interest rates.[15]

- Bonds bought before May 1997 earn different interest rates depending on when they were bought.

- Bonds bought between May 1997 and April 2005 earn a variable interest rate, meaning their interest rate changes. It changes every 6 months and it's 90% of the average 5-year Treasury yield for the previous 6 months.

- Bonds bought between May 2005 and the end of 2006 earn between 3.2 percent and 3.7 percent interest and will continue to do so for as long as you own them.

Community Q&A

-

QuestionDo you get penalized for cashing savings bonds?

wikiHow Staff EditorThis answer was written by one of our trained team of researchers who validated it for accuracy and comprehensiveness.

wikiHow Staff EditorThis answer was written by one of our trained team of researchers who validated it for accuracy and comprehensiveness.

Staff AnswerwikiHow Staff EditorStaff AnswerYou don’t get penalized, but you may have to pay taxes on any interest accrued. You also have the option to pay taxes on interest every year so you don’t have to pay it out in one lump sum when you cash in the bond. In some cases, you can avoid paying taxes on your interest—for example, if you use the bond to pay for higher education expenses like tuition and fees. -

QuestionCan you cash savings bonds at any bank?wikiHow Staff EditorThis answer was written by one of our trained team of researchers who validated it for accuracy and comprehensiveness.

Staff AnswerwikiHow Staff EditorStaff AnswerMost banks in the U.S. will cash your EE savings bond. If you’re not a customer at the bank, you won’t be able to cash a bond worth more than $1000. Be prepared to show your ID so the bank can verify that you’re the owner of the bond. -

QuestionDo I have to pay taxes on my bond when I cash it in?wikiHow Staff EditorThis answer was written by one of our trained team of researchers who validated it for accuracy and comprehensiveness.

Staff AnswerwikiHow Staff EditorStaff AnswerYes, you will need to pay federal income taxes on your bond. However, you have a choice to pay taxes on your interest every year or defer until you actually cash in the bond.

Warnings

- If you are under 18, you can redeem your savings bonds but only with the help of your parent or legal guardian. If you have an electronic bond, it will be linked in the parent or guardian’s TreasuryDirect account. If you have a paper bond, your parent or guardian must accompany you to the bank to redeem it.[17]⧼thumbs_response⧽

References

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://treasurydirect.gov/indiv/research/indepth/smartexchangeinfo.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem_disaster.htm

- ↑ https://www.treasurydirect.gov/indiv/research/sigcert.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eedeath.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eetaxconsider.htm

- ↑ https://www.usnews.com/education/best-colleges/paying-for-college/articles/2017-02-01/pros-cons-of-paying-for-college-with-savings-bonds

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeratesandterms.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem.htm

- ↑ https://www.treasurydirect.gov/indiv/research/indepth/ebonds/res_e_bonds_eeredeem_special.htm

About This Article

To cash in series EE savings bonds, you'll need to wait at least 1 year after you purchased the bond or received it as a gift. However, you might want to wait 5 years to cash in your bond since you'll lose the last 3 months of interest if you cash it in before then. When you're ready to cash in your bond, you'll need to visit a bank in your area that redeems EE savings bonds. Or, if you have an electronic bond, you can redeem it online through the TreasuryDirect website. To learn how to redeem lost, stolen, or destroyed bonds, scroll down!