This article was co-authored by Michael R. Lewis. Michael R. Lewis is a retired corporate executive, entrepreneur, and investment advisor in Texas. He has over 40 years of experience in business and finance, including as a Vice President for Blue Cross Blue Shield of Texas. He has a BBA in Industrial Management from the University of Texas at Austin.

wikiHow marks an article as reader-approved once it receives enough positive feedback. In this case, several readers have written to tell us that this article was helpful to them, earning it our reader-approved status.

This article has been viewed 348,141 times.

Goodwill is a type of intangible asset that may arise when a company acquires another company entirely. Because acquisitions are designed to increase the value of the combined firm, the purchase price paid often exceeds the book value of the acquired company. This gap between the book value and the price is referred to as goodwill, and is necessary to keep the parent company's books balanced. Learning how to account for goodwill will allow you to account properly for acquisitions.

Steps

Understanding Goodwill

-

1Recognize the difference between tangible and intangible assets. Goodwill is considered an intangible asset. Unlike tangible assets, which are physical assets such as property, machinery, or vehicles, an intangible asset is an asset that cannot be touched. These would traditionally include things like brand names, copyrights, patents, or trademarks.[1]

- From an accounting perspective, both tangible and intangible assets are recorded on the balance sheet, since both types of assets have value.

-

2Calculate the book value of a company. Understanding goodwill requires an understanding of book value. Book value is the tangible assets of a business minus its liabilities (also known as its debt and its intangible assets). It is called book value because this is the value of the business that is being carried on the balance sheet.[2]

- For example, assume there is a business with tangible assets of $2 million, intangible assets of $500 thousand, and liabilities of $1 million. This would mean the book value is equal to $1 million ($2 million of tangible assets minus $1 million of liabilities).

- The value of business's assets are equal to the cost that was originally paid for them.

- Note that the book value of the business is not necessarily equal to the market value (also known as fair value) of the business, or what the market would be willing to pay. For example, the above business has a book value of $1 million, but the market may be willing to pay $3 million.

Advertisement -

3Learn the definition of goodwill. When a business is purchased, goodwill is equal to the amount the purchase price is above the book value of the business.

- For example, pretend Company A wants to buy Company B for $1 million. Assume the book value of Company B is $500,000. Since goodwill is equal to the amount the purchase exceeds the book value, the goodwill in this case would equal $500,000.

- Goodwill can exist for many reasons. A business may be willing to pay more than the book value because the business in question may have great profit margins, exceptional future profit growth prospects, or a major competitive advantage.

Accounting for Goodwill

-

1Determine the fair value of the company's assets. As mentioned earlier, the book value of a business does not always equal the market value (the fair value, or, the estimated value that someone in the market would pay for the business). The first step is to take the book value of the business (or the assets minus the liabilities), and figure out what the market value of those net assets are.

- For example, the book value of the business being purchased may be $1 million. However, due to recent strong market conditions, the market value may be slightly higher, at $1.5 million. This means people would pay $1.5 million for those $1 million in assets.

- Calculating market value is usually fairly complex and requires plenty of background knowledge, and as a result, the fair value of a business is usually calculated by a certified professional, such an accountant, financial analyst, or appraiser.

- Typically, figuring out market value will involve looking at what other similar assets or businesses are selling for. One approach is to average the value of similar businesses being sold, and then price the value of the business being purchased above or below the average depending on the quality of the business.

- The term "market value" is interchangeable with "fair value" for the purpose of this article.

-

2Add together the values of all acquired assets. Once the fair value of assets has been determined, you can add them together. For example, assume the business being purchased has $200,000 in property, plant, and equipment, $500,000 in cash, and $800,000 in inventory.

- The fair value of the business's assets would therefore be $1.5 million.

-

3Subtract the business's liabilities from the assets. If the business has liabilities of $500,000, subtracting this from the business's assets of $1.5 million means the fair value of the company's assets is $1 million.

- This simply means that if you subtract the business's assets from their liabilities to get a book value, and you determine what the market would pay in theory for those assets, the result in this case would be $1 million.

-

4Subtract the book value from the purchase price to calculate Goodwill. Goodwill is defined as the price paid in excess of the firm's fair value. To calculate it, simply subtract the total asset market value amount from the purchase price; this amount is nearly always a positive number.

- For example, consider a firm that acquires another firm for $1,000,000. If the book value of the acquired firm totals $800,000, then the amount of goodwill realized is (1,000,000 - 800,000) or $200,000.

-

5Record the journal entry to recognize the acquisition. Once the amount of Goodwill is determined, open whatever accounting software you use to enter the appropriate general entries.

- Continuing with the above example, the firm would credit the acquired asset account for $800,000, credit Goodwill for $200,000, and debit the Cash account for $1,000,000. Goodwill is an intangible asset account on the balance sheet.

- This series of entries adds the $800,000 in assets to the books, adds the $200,000 in Goodwill, and subtracts $1 million in cash from the books to reflect cash leaving to fund the purchase.

-

6Test the goodwill account for impairment each year. Each year, Goodwill needs to be tested for something known as impairment. Impairment occurs when something bad happens to a business, which causes the market value of it's assets to decline below the book value. When this happens, Goodwill needs to be reduced by the amount the market value falls below the book value.

- For example, assume you made a purchase for $1.5 million, where $500,000 is Goodwill, and the book value of the assets are $1 million. If sales drop dramatically, those $1 million of assets will not have a market value of $1 million anymore. If the market value drops to $800,000, would would need to reduce Goodwill by $200,000 to reflect the drop in the value of the assets.

-

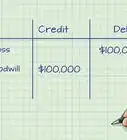

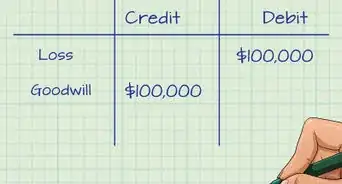

7Record the journal entry to recognize any goodwill impairment. If the goodwill account needs to be impaired, an entry is needed in the general journal. To record the entry, credit Loss on Impairment for the impairment amount and debit Goodwill for the same amount. This accounts for a reduction in Goodwill by using Loss on Impairment as a contra-asset account.

References

About This Article

To account for goodwill, calculate how much you have by subtracting the fair market value from the purchase price. So, if you bought a company for $1,000 when it’s fair market value is $800, you would have $200 in goodwill. Then, each year you have to determine if people are willing to pay less for the company than you have stored in it. For example, if the company has $1,000 in assets, but people will only pay $900 for it, then you’d have to subtract $100 from the goodwill. Keep reading for advice from our Financial reviewer on how to calculate fair market value!