Defining Operating Leverage

Operating leverage can be defined, simply, as the degree to which a firm incurs a combination of fixed and variable costs. Specifically, it is the use of fixed costs over variable costs in production. For example, replacing production workers (variable cost) with robots (fixed cost) . Operating leverage is also a measure of how revenue growth translates into growth in operating income.

Example of Operating Leverage

Factory automation with industrial robots for metal die casting.

Recall that variable costs are those that change alongside the volume activity of a business, and fixed costs are those that remain constant regardless of volume. Utilizing operating leverage will allow variable costs to be reduced in favor of fixed costs; therefore, profits will increase more for a given increase in sales. This is, of course, after the breakeven point has been reached. In other words, because variable costs are reduced, each sale will contribute a higher profit margin to the company.

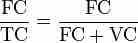

Fixed and Variable Costs

Fixed costs and variable costs, together, comprise total costs.

As operating leverage increases, more sales are needed to cover the increased fixed costs. Therefore, companies with low output would not benefit from increased operating leverage. Moreover, high levels of fixed costs increase business risk, which is the inherent uncertainty in the operation of the business. Manufacturing companies tend to invest heavily in fixed assets. Therefore, operating leverage is used much more than financial leverage for these types of firms. Operating leverage also increases forecasting risk. Therefore, even a small error made in forecasting sales can be magnified into a major error in forecasting cash flows.

Interpreting Operating Leverage

Various measures can be used to interpret operating leverage. These include the ratio of fixed costs to total costs, the ratio of fixed costs to variable costs, and the Degree of Operating Leverage (DOL). All of these measures depend on sales. The ratios of fixed cost to total costs and fixed costs to variable costs tell us that if the unit variable cost is constant, then as sales increase, operating leverage decreases. The DOL tells us, as a percentage, that for a given level of sales and profit, a company with higher fixed costs has a higher contribution margin - the marginal profit per unit sold. Therefore, its operating income increases more rapidly with sales than a company with lower fixed costs (and correspondingly lower contribution margin).