A fundamental concept in economics is that of scarcity. In contrast to its colloquial usage, scarcity in economics connotes not that something is nearly impossible to find, but simply that it is not unlimited. For example, the number of available hours in a day is a scarce resource: there is a finite amount of time available to you to do work, hang out with friends, and relax. Most resources are scarce in most situations.

Since resources tend to be scarce, anyone that uses the resource has to make a decision about how to use it. Suppose, for example, that you are a drink manufacturer. To produce a beverage, you have to use some scarce resources: the plastic for the bottle, the workers' time, a machine to fill the bottles, etc. If you choose to make one bottle of water, you have chosen to not make a bottle of soda . Your scarce resources force you to make a choice and a trade-off producing one product or another.

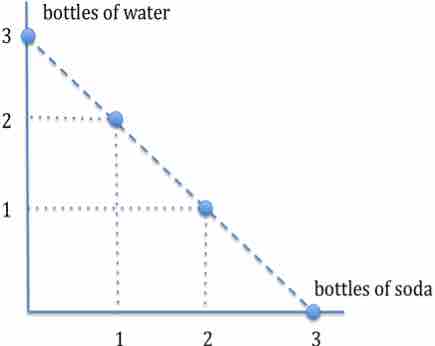

Tradeoffs

Since resources are scarce for a drink manufacturer, it must make a tradeoff between producing bottles of water and bottles of soda.

Like producers, consumers also have to make choices. Often, consumer must choose between current consumption ("I want to buy an ice cream") and future consumption ("I should rather save my money so I can buy an ice cream tomorrow"). Since consumers' resources such as time, attention, and money are limited, they must choose how to best allocate them by making tradeoffs.

The concept of trade-offs due to scarcity is formalized by the concept of opportunity cost. The opportunity cost of a choice is the value of the best alternative forgone. In other words, if you can only produce bottles of soda and water, the opportunity cost of producing a bottle of water is the value of producing a bottle of soda. Similarly, there is an opportunity cost in everything: the opportunity cost of you reading this is what you could be doing with your time instead (say, watching a movie). When scarce resources are used (and just about everything is a scarce resource), people and firms are forced to make choices that have an opportunity cost.