Monopoly Production

A pure monopoly has the same economic goal of perfectly competitive companies - to maximize profit. If we assume increasing marginal costs and exogenous input prices, the optimal decision for all firms is to equate the marginal cost and marginal revenue of production. Nonetheless, a pure monopoly can – unlike a firm in a competitive market – alter the market price for its own convenience: a decrease of production results in a higher price. Because of this, rather than finding the point where the marginal cost curve intersects a horizontal marginal revenue curve (which is equivalent to good's price), we must find the point where the marginal cost curve intersect a downward-sloping marginal revenue curve.

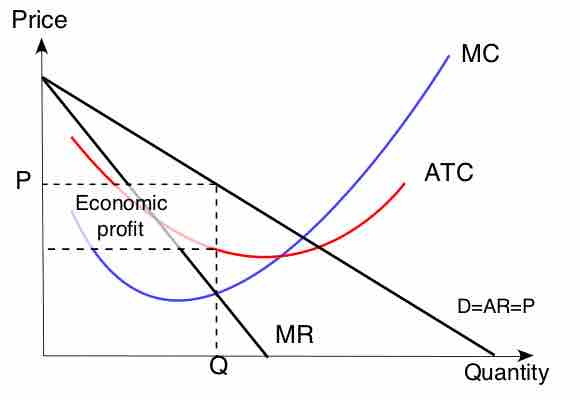

Monopoly Production Point

Like non-monopolies, monopolists will produce the at the quantity such that marginal revenue (MR) equals marginal cost (MC). However, monopolists have the ability to change the market price based on the amount they produce since they are the only source of products in the market. When a monopolist produces the quantity determined by the intersection of MR and MC, it can charge the price determined by the market demand curve at the quantity. Therefore, monopolists produce less but charge more than a firm in a competitive market .

Monopoly Production

Monopolies produce at the point where marginal revenue equals marginal costs, but charge the price expressed on the market demand curve for that quantity of production.

In short, three steps can determine a monopoly firm's profit-maximizing price and output:

- Calculate and graph the firm's marginal revenue, marginal cost, and demand curves

- Identify the point at which the marginal revenue and marginal cost curves intersect and determine the level of output at that point

- Use the demand curve to find the price that can be charged at that level of output