The concept of budget constraints in the field of economics revolves around the idea that a given consumer is limited in consumption relative to the amount of capital they possess. As a result, consumers analyze the optimal way in which to leverage their purchasing power to maximize their utility and minimize opportunity costs. This is achieved through using budget constraints, which represent the plausible combinations of products and/or services a buyer is capable of purchasing with their capital on hand.

Trade-offs

To expand upon this definition further, the business concept of opportunity cost via trade-offs is a central building block in understanding budget constraints. An opportunity cost is defined as the foregone value of the next best alternative in a given action. To apply this to a real-life situation, pretend you have $100 to spend on food for the month. You have a wide variety of options, but some will provide you with higher opportunity costs than others. You could purchase enough bread, rice, milk and eggs to feed yourself for the full month or you could buy premium cut steak and store-prepared dinners by the pound (which would last about one week). The opportunity cost of the former is the high quality foods which have the convenience factor of already being prepared for you while the opportunity cost of the latter is having enough food to feed yourself for the entire month. In this circumstance the decision is easy, and the trade off will be sacrificing convenience and high quality food for the ability to have enough food on the table over the course of the whole month.

Budget Curves and Indifference Curves

Understanding these trade-offs underlines the true function of budget constraints in economics, which is identifying which consumer behaviors will maximize utility. Consumers are inherently equipped with an infinite demand and a finite pool of resources, and therefore must make budgetary decisions based on their preferences. The way economists demonstrate this arithmetically and visually is through generating budget curves and indifference curves.

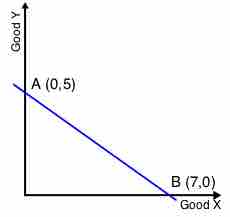

Budget curves: This indicates the relationship between two goods relative to opportunity costs, which defines the value of each good relative to one another. For example, on the figure provided a quantity of 5 for 'good

Budget Curve

A budget curve demonstrates the relationship between two goods relative to opportunity costs, essentially deriving the relative value of each good based on quantity and utility. Keep in mind that moving from one point on the in to another is trading off '

Indifference curves: Indifference curves underline the way in which a given consumer interprets the value of each good relative to one another, demonstrating how much of 'good

Indifference Curves

Indifference curves are designed to represent an equal perception of overall value in a given basket of goods relative to a specific consumer. That is to say that each point along the curve is considered by the consumer of equivalent value despite alterations in the quantity of each good, as these trade-offs are consider of equal value and thus indifferent.

Through utilizing these economic tools, economists can predict consumer behavior and consumers can maximize their overall utility based upon their budget constraints.