The long-run is the period of time where there are no fixed variables of production. As with any other economic equilibrium, it is defined by demand and supply.

Demand

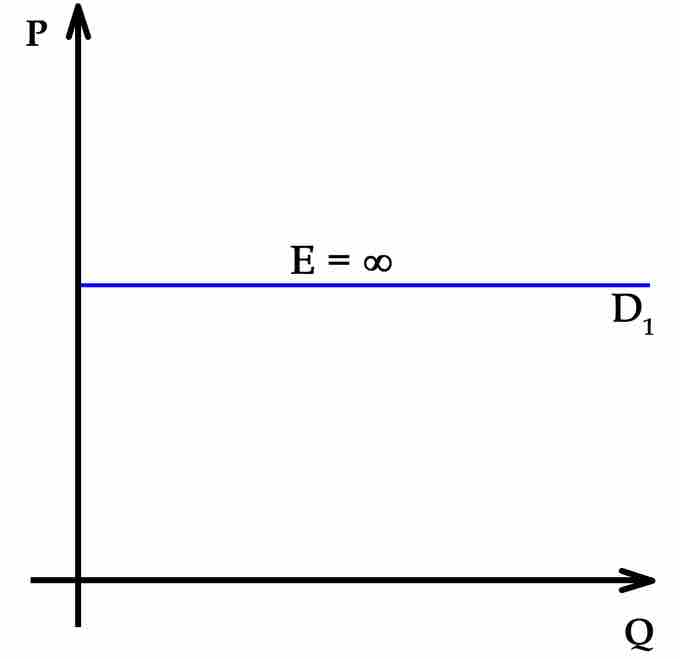

In a perfect market, demand is perfectly elastic . The demand curve also represents marginal revenue, which is important to remember later when we calculate quantity supplied. That means regardless of how much is produced by the suppliers, the price will remain constant.

Perfectly Elastic Demand

In a perfectly competitive market, demand is perfectly elastic.

Supply

In a perfectly competitive market, it is assumed that all of the firms participating in production are trying to maximize their profits. So a firm will produce goods until the marginal costs of production equal the marginal revenues from sales. In a perfectly competitive market in the long-term, this is taken one step further. In a perfectly competitive market, long-run equilibrium will occur when the marginal costs of production equal the average costs of production which also equals marginal revenue from selling the goods. So the equilibrium will be set, graphically, at a three-way intersection between the demand, marginal cost and average total cost curves.

Repercussions of Equilibrium

A perfectly competitive market in equilibrium has several important characteristics.

- Firms can't make economic profit; the best they can do is break even so that their revenues equals their costs.

- The market is productively and allocatively efficient. This means that not only is the market using all of its resources efficiently, it is using its resources in a way that maximizes the social welfare.

- Economic surplus is maximized, which means there is no deadweight loss. Attempting to improve the conditions of one group would harm the interests of the other.