Economic Equilibrium

In economics, equilibrium is a state where economic forces (supply and demand) are balanced. Without any external influences, price and quantity will remain at the equilibrium value .

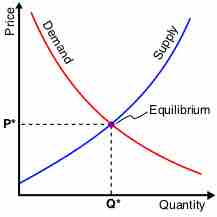

Equilibrium

Similar to microeconomic equilibrium, the macroeconomic equilibrium is the point at which the aggregate supply intersects the aggregate demand.

Supply and Demand

Determining the supply and demand for a good or services provides a model of price determination in a market. In a competitive market, the unit price for a good will vary until it settles at a point where the quantity demanded equals the quantity supplied. The result is the economic equilibrium for that good or service.

There are four basic laws of supply and demand. The laws impact both supply and demand in the long-run.

- If quantity demand increases and supply remains unchanged, a shortage occurs, leading to a higher price until the quantity demanded is pushed back to equilibrium.

- If quantity demand decreases and supply remains unchanged, a surplus occurs, leading to a lower price until the quantity demanded is pushed back to equilibrium.

- If quantity demand remains unchanged and supply increases, a surplus occurs, leading to a lower price until the quantity supplied is pushed back to equilibrium.

- If quantity demand remains unchanged and supply decreases, a shortage occurs, leading to a higher price until the quantity supplied is pushed back to equilibrium.

Aggregate Supply and Aggregate Demand

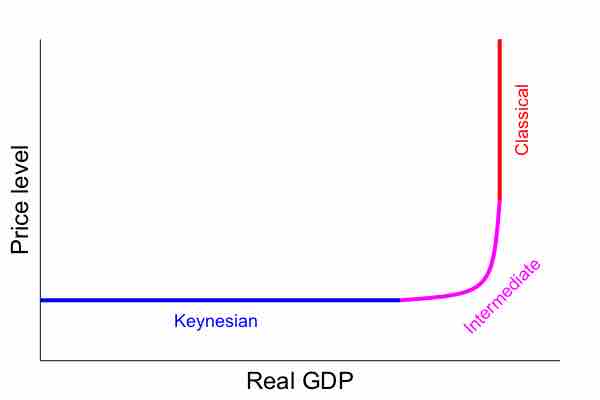

Aggregate supply is the total supply of goods and services that firms in a national economy plan on selling during a specific time period. It is the total amount of goods and services that firms are willing to sell at a specific price level in an economy .

Aggregate supply

This graph shows the three stages of aggregate supply. It is the total supply of goods and services that firms in a national economy plan to sell during a specific time period. Changes in aggregate supply cause shifts along the supply curve.

Aggregate demand is the total demand for final goods and services in an economy at a given time and price level. It is the demand for the gross domestic product (GDP) of a country.

Aggregate Supply-Aggregate Demand Model

Equilibrium is the price-quantity pair where the quantity demanded is equal to the quantity supplied. It is represented on the AS-AD model where the demand and supply curves intersect. In the long-run, increases in aggregate demand cause the price of a good or service to increase. When the demand increases the aggregate demand curve shifts to the right. In the long-run, the aggregate supply is affected only by capital, labor, and technology. Examples of events that would increase aggregate supply include an increase in population, increased physical capital stock, and technological progress. The aggregate supply determines the extent to which the aggregate demand increases the output and prices of a good or service.

When the aggregate supply and aggregate demand shift, so does the point of equilibrium. The aggregate demand curve shifts and the equilibrium point moves horizontally along the aggregate supply curve until it reaches the new aggregate demand point.