Open Economy

In an open economy there there is a flow of funds across borders due to the exchange of goods and services. An open economy can import and export without any barriers to trade, such as quotas and tariffs. Citizens in a country with an open economy typically have access to a larger variety of goods and services. They also have the ability to invest savings outside of the country.

An open economy allows a country to spend more or less than what it earns through the output of goods and services every year. When a country spends more than it make, it borrows money from abroad. If a country saves more money than it makes, it can lend the difference to foreigners.

The equation used to determine the economic output of a country is

The economy's output (Y) equals the sum of the consumption of domestic goods (Cd), the investment in domestic goods and services (Id), the government purchase of domestic goods and services (Gd), and the net exports of domestic goods and services (NX). The sum of C, I, and G provides the domestic spending of a country, while X provides the foreign sources of spending.

The amount that a country saves is total of investment and net exports:

NX can also be considered the trade balance of a country. Therefore

Consider, for example, what happens if domestic interest rates rise relative to foreign interest rates. Savings will increase and investment will drop as investors borrow and invest abroad instead. The balance of trade will increase, affecting the health of the economy. In an open economy, market actors can choose to save, spend, and invest either domestically or internationally, so relative changes affect not only the flow of capital, but also the health of the economy as a whole.

Economic Equilibrium

In an open economy, equilibrium is achieved when supply and demand are balanced . When no external influences are present, the state of equilibrium between the variables will not change. In the case of market equilibrium in an open economy, equilibrium occurs when a market price is established through competition. For example, when the amount of goods and services sought by buyers is equal to the amount of goods and services produced by sellers. When equilibrium is reached and the market price is established in an open economy, the price of the goods or service will remain the same unless the supply or demand changes.

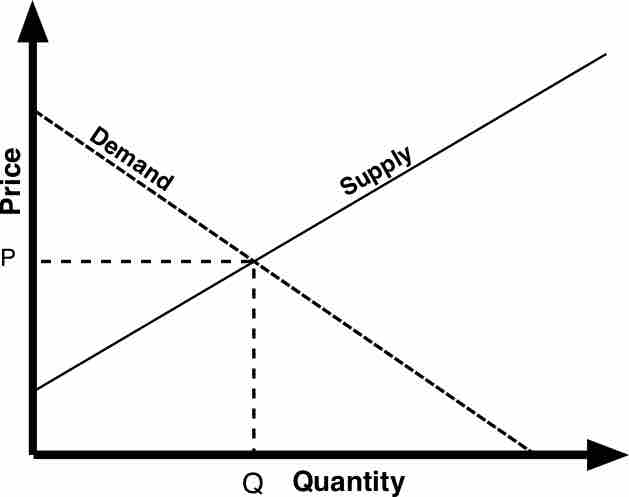

Equilibrium

The graph shows that the point of equilibrium is where the supply and demand are equal. In an open economy, equilibrium is achieved when the amount demanded by consumers is equal to the amount of a goods or service provided by producers.

There are three properties of equilibrium:

- The behavior of agents is consistent,

- No agent has an incentive to change its behavior, and

- Equilibrium is the outcome of some dynamic process (stability).

In an open economy, equilibrium is reached through the price mechanism. For example, if there is excess supply (market surplus), this would lead to prices cuts which would decrease the quantity supplied (reduces the incentive to produce and sell the product) and increase the quantity demanded (by offering bargains), which would eliminate the original excess of supply. The interest rates also adjust to reach equilibrium. Although consumption does not always equal production, the net capital outflow does equal the balance of trade. The capital flows, which depend on interest rates and savings rates, also adjust to reach equilibrium.