Marginal Cost

Marginal cost is the change in the total cost that occurs when the quantity produced is increased by one unit . It is the cost of producing one more unit of a good. When more goods are produced, the marginal cost includes all additional costs required to produce the next unit. For example, if producing one more car requires the building of an additional factory, the marginal cost of producing the additional car includes all of the costs associated with building the new factory.

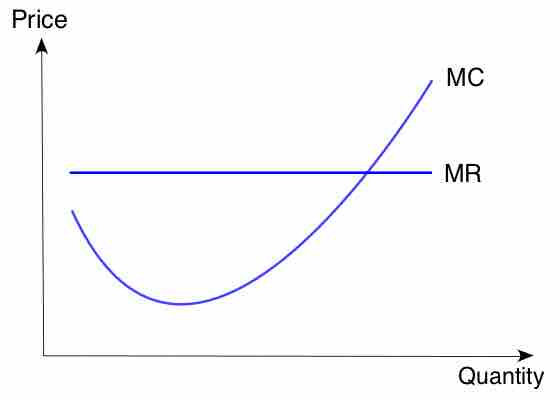

Marginal cost curve

This graph shows a typical marginal cost (MC) curve with marginal revenue (MR) overlaid.

Marginal cost is the change in total cost divided by the change in output.

An example of marginal cost is evident when the cost of making one pair of shoes is $30. The cost of making two pairs of shoes is $40. Therefore the marginal cost of the second shoe is $40 -$30=$10.

Marginal Revenue

Marginal revenue is the additional revenue that will be generated by increasing product sales by one unit. In a perfectly competitive market, the price of the product stays the same when another unit is produced. Marginal revenue is calculated by dividing the change in total revenue by the change in output quantity.

For example, if the price of a good in a perfectly competitive market is $20, the marginal revenue of selling one additional unit is $20.

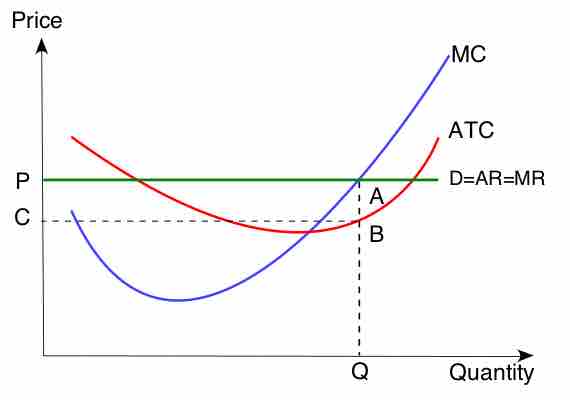

Marginal Cost-Marginal Revenue Perspective

Profit maximization is the short run or long run process by which a firm determines the price and output level that will result in the largest profit. Firms will produce up until the point that marginal cost equals marginal revenue. This strategy is based on the fact that the total profit reaches its maximum point where marginal revenue equals marginal profit . This is the case because the firm will continue to produce until marginal profit is equal to zero, and marginal profit equals the marginal revenue (MR) minus the marginal cost (MC).

Marginal profit maximization

This graph shows profit maximization using the marginal cost perspective.

Another way of thinking about the logic is of producing up until the point of MR=MC is that if MR>MC, the firm should make more units: it is earning a profit on each. If MR<MC, then the firm should produce less: it is making a loss on each additional product it sells.